Financing primitive

What is Fractals?

A financing primitive for the infrastructure of the next economy.

Built on Solana

Productive infra, no rails

On-chain cash-flow claim

On-chain rewards today

Any orphaned yield shape

Overview

Why this exists

There is a category of infrastructure being built right now that the existing capital system cannot finance — and it is going to be the most important category of the next twenty years.

It is distributed where traditional infrastructure is centralized. It is operated by tens of thousands of small participants where traditional infrastructure is operated by a handful of large ones. It is small at the unit level, atomic in nature.

The wireless networks deploying at the edge. The energy systems on residential rooftops. The compute clusters in distributed datacenters. The sensors covering roads, skies, and farms. The chargers, the screens, the machines — the small-format operators that will populate the physical world as it gets instrumented and intelligent. This is not speculative. It is the working substrate of how the next economy functions, and most of it is being built right now.

The existing capital system does not know how to finance nor coordinate its buildout.

Private credit is too slow and too concentrated. Venture capital funds the platforms above this infrastructure but ignores the unit-level deployments below. Public equity will not underwrite anything below a billion in revenue. Bank debt demands collateral profiles small operators cannot produce. Each individual deployment is too small for institutional capital, too unconventional for traditional debt, and too distributed for any of them. The operators building this infrastructure mostly hit the same wall: the unit economics work, and no one will write the check.

Section 01

The gap

The result is a structural gap — and the gap is enormous. On one side: more idle, yield-seeking on-chain capital than at any point in history. Stablecoin supply outstanding crossed $175 billion, and the overwhelming majority of yield available to that capital is recursive — borrowed against itself, looped against itself, paid out by other crypto rather than by productive activity outside of it.

On the other side: more underfinanced productive infrastructure than at any point in history, sitting in operators' pipelines waiting for capital that existing channels will not deliver.

Neither side can reach the other through the rails that exist.

We are building the rail

Fractals is the connection between on-chain capital and productive physical infrastructure — starting where the mechanism is clearest and scaling across every category the existing system cannot reach.

Section 02

The instrument

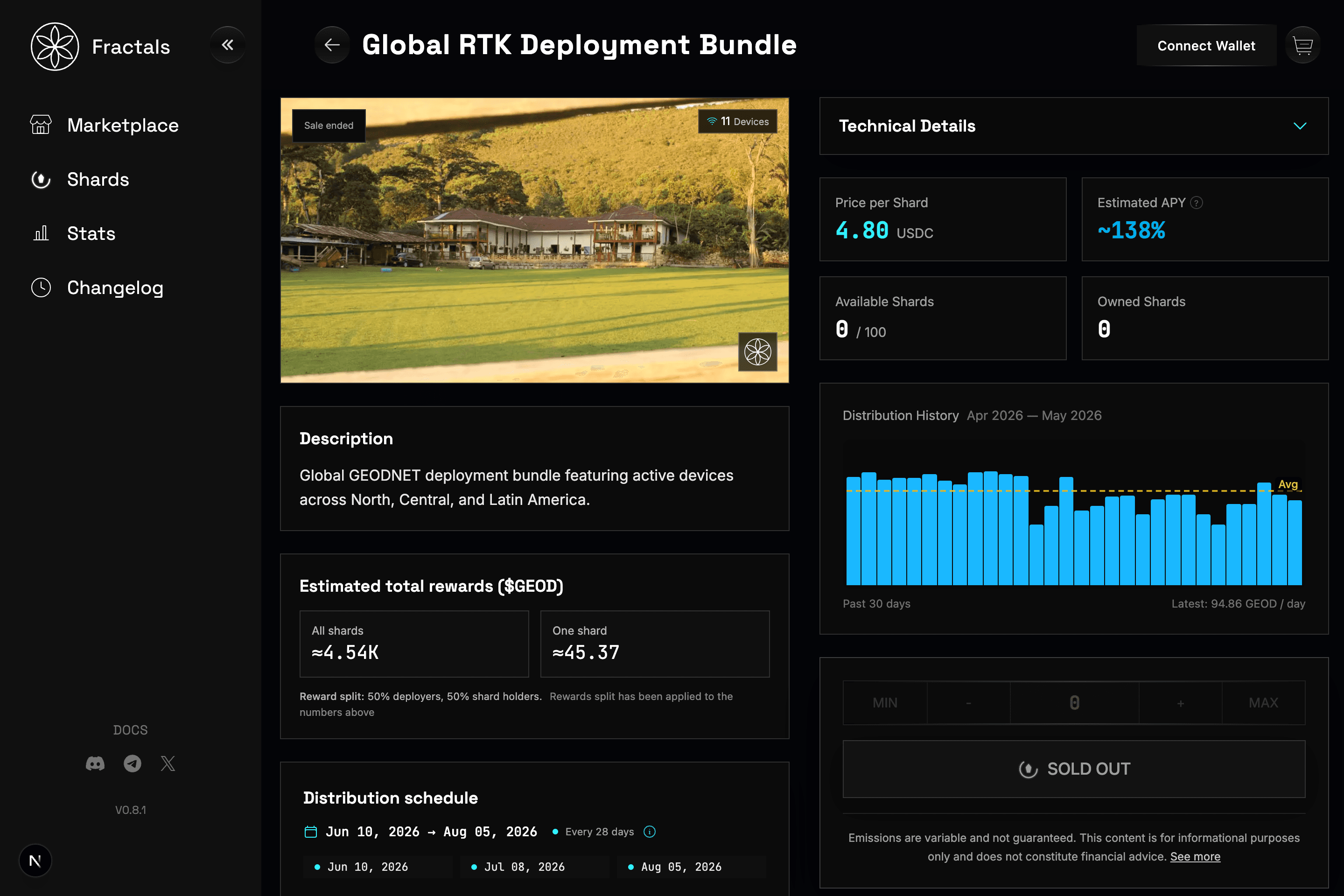

A Shard is an on-chain, transferable, fractional claim on the future cash flows of a productive asset. The asset can be one device or a pool of them. The cash flow can be paid in tokens or dollars. The buyer can be retail or institutional. The instrument is settled on Solana, backed by real instrument law in the underlying entity, and built to compose with the rest of on-chain finance.

That is the primitive. Everything else is a structure built on top of it.

The same underlying brick can be assembled into many different financial products. A single Shard can represent a claim on one specific deployment. A bundle of Shards can represent diversified exposure across a fleet — across operators, geographies, and asset types. A tranched offering can split cash flows into senior, mezzanine, and equity layers, each priced for a different buyer. A leveraged product can amplify exposure using underlying cash flows as collateral. An indexed product can give a single token exposure to a basket of deployments across an entire vertical.

This is what makes Shards a primitive rather than a product. They are the unit out of which infrastructure financing markets get built — the way bonds are the unit out of which credit markets get built. The instrument is general. The applications are not.

Devices bundled for sale with terms and payout plan

Fractional on-chain claim on future cash flows

Scheduled reward payouts to shard holders

Browse, compare, and purchase shards

Section 03

DePIN is the wedge

The first version of any general-purpose financing primitive needs a wedge — a category where the mechanism is clearest, participants are most ready, and the technical surface is smallest. For Fractals, that wedge is DePIN.

Decentralized physical infrastructure networks — Helium, GEODNET, Hivemapper, XNET, and the rest of the protocols deploying real hardware that earns on-chain rewards — are the easiest category to finance with Shards. Cash flows are already on-chain. Operators already run wallets. Deployments are already happening. Many protocols have stopped being speculative and started being real businesses, with verifiable revenue at multi-million-dollar run rates. They need capital to keep deploying. They have no good way to get it.

We start there because that is where conversion is most direct. A Shard against a Helium hotspot or a GEODNET reference station is the simplest expression of the primitive: future on-chain rewards routed pro-rata to Shard holders, with Nexus underwriting location and venue before listing. The mechanism works end-to-end. Buyers earn real yield. Operators get real capital. The network grows.

DePIN is the smallest version of what this is.

Section 04

What this becomes

The same Shard primitive applies to any cash-flow-generating asset that is small at the unit level, distributed across many operators, and structurally orphaned by traditional capital. Most of it has nothing to do with crypto.

EV charging networks where unit economics work per charger but no fund will finance one charger at a time. ATM fleets with steady cash flow but operators running eight machines, not eight hundred. Vending. Parking. Digital out-of-home advertising. Cold storage. Last-mile delivery hubs. Residential solar. Cell towers and small-cell deployments telco capex won't reach. Robots, edge compute, and small-scale automation as the physical world gets instrumented — and frontier categories not named yet because they have not been built yet.

What unites them is not the technology. It is the financing shape: yield-producing infrastructure with real unit economics and no efficient way to access capital — things the existing system leaves on the table.

Through a fiat-to-USDC bridge — operationally routine through Mercury, Circle, and the broader stablecoin onramp stack — any of these can be financed through the same Shard primitive that finances DePIN today. The mechanism does not care whether cash flow originates as HNT or as US dollars. It cares whether cash flow is measurable, the asset is custodiable, and the operator is real. Most useful infrastructure satisfies those three.

That is why Fractals is described as a financing primitive for the next economy rather than a DePIN tool or a yield product. Those frames are too narrow. What is being built is the rail by which on-chain capital reaches productive infrastructure across every category where capital can earn a real return and infrastructure can find a real buyer.